Master the Art of Endorsing Checks to Boost Your Business Revenue

In today’s digital age, many business owners assume that paper checks are becoming obsolete. However, checks remain a significant part of business transactions, with billions of checks processed annually in the United States. Understanding how to properly endorse checks is not just a basic business skill—it’s a critical component of revenue management that can directly impact your cash flow and financial operations.

Proper check endorsement ensures that your business receives payments securely and efficiently while maintaining compliance with banking regulations. Whether you’re dealing with customer payments, vendor refunds, or business-to-business transactions, mastering the art of check endorsement can streamline your revenue collection process and protect your business from potential financial risks.

Understanding Check Endorsement Fundamentals

A check endorsement is your signature or stamp on the back of a check that legally transfers ownership of the funds from the payee to you or your designated recipient. This process is governed by the Uniform Commercial Code (UCC), which establishes the legal framework for negotiable instruments across all U.S. states.

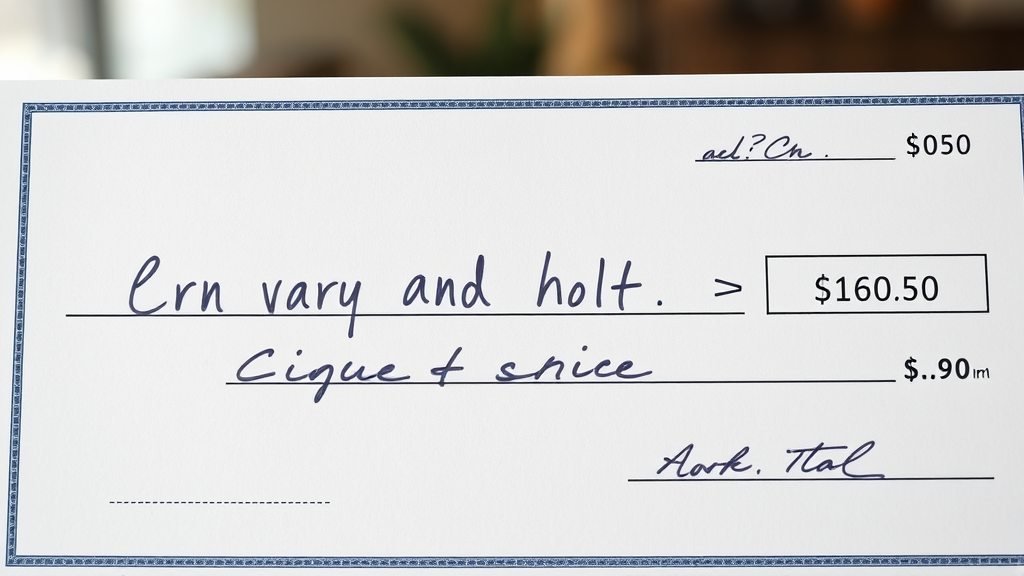

The endorsement area is located on the back of the check, typically within the top 1.5 inches. This space is reserved exclusively for endorsement purposes, and any marks outside this area can cause processing delays or rejections by financial institutions. Understanding this fundamental concept is crucial for maintaining smooth business operations and ensuring that your revenue collection processes remain efficient.

For businesses, check endorsement serves multiple purposes beyond simple ownership transfer. It provides a legal record of the transaction, helps prevent fraud, and ensures compliance with banking regulations. When you endorse a check correctly, you’re essentially providing authorization for the bank to process the payment and credit your business account.

Types of Check Endorsements for Business

Business owners must understand the three primary types of check endorsements, each serving different purposes and offering varying levels of security. The choice of endorsement type depends on your specific business needs, security requirements, and the method of deposit.

Blank Endorsement

A blank endorsement consists of simply signing your name (or stamping your business name) on the back of the check. This type of endorsement makes the check payable to anyone who possesses it, essentially converting it into cash. While this is the quickest method, it’s also the least secure and should only be used when depositing checks immediately at the bank.

Restrictive Endorsement

A restrictive endorsement limits how the check can be used by adding specific instructions along with your signature. The most common restrictive endorsement for businesses is “For Deposit Only” followed by your account number and signature. This prevents anyone else from cashing the check if it’s lost or stolen, making it the preferred method for most business transactions.

Special Endorsement

A special endorsement allows you to transfer the check to another person or entity by writing “Pay to the order of [Name]” followed by your signature. This type is useful when you need to endorse a check over to a business partner, vendor, or another party, though it requires careful consideration of legal implications.

Step-by-Step Guide to Endorsing Business Checks

Properly endorsing business checks requires attention to detail and adherence to specific procedures. Just as you might need to follow precise steps when learning how to double space in Word for professional documents, check endorsement demands accuracy and consistency.

First, verify that the check is made out correctly to your business name exactly as it appears on your bank account. Any discrepancies could cause processing delays. Turn the check over and locate the endorsement area, which is typically marked by lines or a designated box at the top portion of the back.

Write or stamp your endorsement within this area, ensuring all information is legible and complete. If using a restrictive endorsement, write “For Deposit Only” at the top, followed by your business account number, then your authorized signature or business stamp below. Always use blue or black ink to ensure optimal processing by check-scanning equipment.

For businesses handling multiple checks daily, consider investing in a custom endorsement stamp that includes your business name, account number, and “For Deposit Only” restriction. This not only saves time but also ensures consistency and reduces the risk of errors that could delay processing.

Mobile Deposit Endorsement Requirements

Mobile deposit technology has revolutionized how businesses handle check deposits, offering convenience and faster access to funds. However, mobile deposits require specific endorsement procedures that differ slightly from traditional over-the-counter deposits. Most banks require additional text such as “For Mobile Deposit Only” along with your standard endorsement information.

When preparing checks for mobile deposit, ensure the endorsement is written clearly within the designated area, as mobile deposit apps use optical character recognition (OCR) technology to process the information. Poor handwriting or endorsements outside the proper area can result in deposit rejections, similar to how technical issues might require you to understand how to recall an email in Outlook when business communications go wrong.

Many financial institutions have specific mobile deposit limits and hold policies that can affect your business cash flow. Understanding these requirements and planning accordingly can help optimize your revenue management processes and ensure faster access to deposited funds.

Business Best Practices and Security Measures

Implementing robust security measures around check endorsement protects your business from fraud and ensures smooth financial operations. Establish clear policies for who can endorse checks on behalf of your business, and maintain a log of all endorsed checks with details including date, amount, and the person responsible for the endorsement.

Store unendorsed checks in a secure location, preferably a locked filing cabinet or safe, and never endorse checks until you’re ready to deposit them. This practice minimizes the risk of loss or theft. Additionally, consider implementing a dual-control system where one person endorses checks and another person verifies the endorsement before deposit.

Regular reconciliation of endorsed checks against deposit records helps identify discrepancies early and maintains accurate financial records. This process should be as systematic as other business procedures, whether you’re managing documents or learning technical skills like how to right click on a Mac for efficient workflow management.

For businesses with multiple locations or employees handling deposits, standardize endorsement procedures across all sites and provide regular training to ensure compliance. Documentation of these procedures should be readily accessible and regularly updated to reflect changes in banking regulations or internal policies.

Common Endorsement Mistakes to Avoid

Several common mistakes can delay check processing or create security vulnerabilities for your business. One frequent error is endorsing checks with incorrect business names or using nicknames instead of the official business name registered with your bank. Always ensure the endorsement matches your account registration exactly.

Another critical mistake is endorsing checks too early in the process. Some business owners endorse checks immediately upon receipt, which creates unnecessary security risks. Best practice dictates endorsing checks only when ready for immediate deposit, similar to how timing matters in other business processes like scheduling texts on iPhone for optimal communication timing.

Illegible endorsements frequently cause processing delays, especially with mobile deposits where OCR technology must accurately read the information. Take time to write clearly or invest in a quality endorsement stamp for consistency. Additionally, placing endorsements outside the designated area can result in check rejection and delayed processing.

Failing to include necessary restrictive language like “For Deposit Only” leaves checks vulnerable to fraud if lost or stolen. This simple addition provides significant protection and should be standard practice for all business check endorsements.

Legal and Regulatory Compliance

Check endorsement practices must comply with federal and state banking regulations, including provisions outlined in the Federal Reserve’s Regulation CC. This regulation governs funds availability and establishes requirements for check processing and endorsement procedures.

The Office of Foreign Assets Control (OFAC) requires businesses to verify that check writers are not on restricted party lists, particularly for international transactions. Maintaining compliance with these regulations protects your business from legal liability and ensures continued banking relationships.

Proper record-keeping of endorsed checks supports compliance efforts and provides necessary documentation for audits or legal proceedings. These records should include copies of endorsed checks, deposit records, and any correspondence related to problem transactions.

Some industries have additional endorsement requirements or restrictions. For example, businesses in heavily regulated sectors may need to maintain enhanced documentation or follow specific endorsement procedures. Consulting with legal counsel or banking professionals ensures your practices meet all applicable requirements.

Frequently Asked Questions

What happens if I endorse a check incorrectly?

If you endorse a check incorrectly, the bank may reject the deposit or place a hold on the funds while they verify the endorsement. Minor errors like slight name variations can often be resolved by providing additional documentation, but significant errors may require obtaining a new check from the payor. Always double-check endorsements before submitting deposits to avoid delays.

Can I endorse a check made out to my business with my personal signature?

You can endorse a business check with your personal signature only if you’re an authorized signatory on the business account. However, it’s best practice to use your business name or an official business stamp to maintain clear separation between personal and business finances. Check with your bank about their specific requirements for business check endorsements.

How long do I have to endorse and deposit a business check?

While checks don’t technically expire, most banks will not honor checks older than six months due to stale-date policies. State laws may provide additional guidelines, but it’s best practice to endorse and deposit business checks within 30-60 days of receipt to ensure smooth processing and maintain good relationships with customers and vendors.

Is a stamp endorsement as legally valid as a handwritten signature?

Yes, endorsement stamps are legally valid and widely accepted by financial institutions when properly executed. Many businesses prefer stamps for consistency and efficiency. However, ensure your stamp includes all necessary information (business name, account number, and any restrictive language) and that only authorized personnel have access to the stamp.

What should I do if I lose an endorsed check before depositing it?

If you lose an endorsed check, immediately contact your bank to report the loss and place a stop-payment alert if possible. Contact the check writer to request a replacement check and provide details about the lost check. If the endorsement included restrictive language like “For Deposit Only,” the risk of fraudulent use is reduced, but prompt action is still essential.

Can I endorse a check electronically for digital deposits?

Electronic endorsement capabilities vary by bank and the type of business account you maintain. Some banks allow digital signatures through their mobile apps or online platforms, while others require physical endorsement even for mobile deposits. Check with your financial institution about their specific electronic endorsement policies and any additional security requirements.

Are there limits on the dollar amount of checks I can endorse for mobile deposit?

Yes, most banks impose daily and monthly limits on mobile deposits, which can range from $2,500 to $25,000 or more depending on your account type and banking relationship. Business accounts typically have higher limits than personal accounts. Large checks may require traditional over-the-counter deposits. Contact your bank to understand your specific limits and procedures for handling large-dollar deposits.

Related Posts

How Long to Boil Lobster Tails: Cooking Guide

How Long to Fly from New York to London? Travel Times